Elevated geopolitical risk around US investment likely to lead to NSIA approval delays and stronger sovereign capability requirements

Executive Summary

US-origin investments in sensitive sectors of the UK economy are likely to come under increasing scrutiny under the UK’s National Security and Investment Act (NSIA) amid heightened geopolitical risk around the US-UK relationship.

NSIA final orders concerning US-origin investments are likely to prioritise measures to protect UK sovereign capability and to limit exposure to US leverage and pricing risk.

Organisations and deal teams should anticipate enhanced scrutiny by introducing protective security measures into companies that mitigate exposure to US-related geopolitical risk.

SECURED is a security consultancy specialising in providing protective security for research and innovation entities of national security significance.

Arrange a rapid review of your organisation’s security posture now.

In December 2025, US data analytics and AI company Palantir technologies secured a GBP240 million agreement with the UK Ministry of Defence (MOD) to support strategic and operational decision making across the UK armed forces and law enforcement agencies [LINK].

The contract was awarded directly, without an option for competition from UK defence firms [LINK], prompting questions about whether the UK is deepening strategic dependence on US technologies at precisely the moment when transatlantic political risk is increasing.

This concern is heightened by the deteriorating relations between the US and Europe under the Trump administration, which has prompted a broader shift among European governments seeking to reduce dependence on US technologies. In January 2026, the French government announced that government departments would transition away from Zoom in favour of a domestic alternative [LINK].

Against this backdrop, it is likely that there will be further scrutiny regarding the UK’s technological and wider strategic dependence on the US, likely extending to how US investment is viewed in the 17 sensitive sectors of the economy covered by the 2021 National Security Investment Act (NSIA).

What does US investment into the NSIA sectors look like currently?

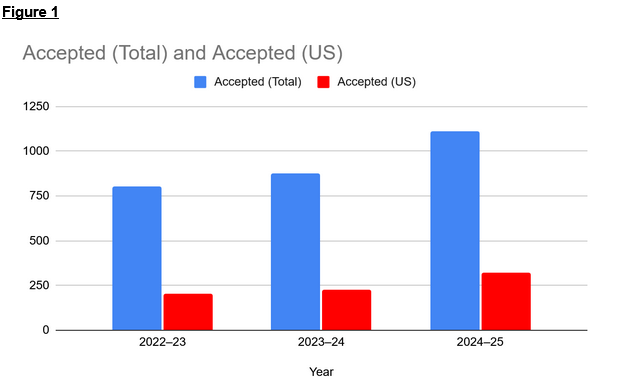

US-origin investments were the second-largest source of notified transactions after UK-origin investments, accounting for between 25% and 29% of all accepted notifications, according to data from the 2022-23, 2023-24, and 2024-25 NSIA annual reports [LINK, LINK, LINK]. Accepted notifications refer to transactions that have been formally submitted to the government for review under NSIA.

Between 2022 and 2025, US-origin accepted notifications increased by 66%, rising from 202 to 322 as displayed in Figure 1 [LINK, LINK, LINK]. This growth occurred alongside a broader increase in accepted notifications, which grew from 806 to 1,110 in the same period.

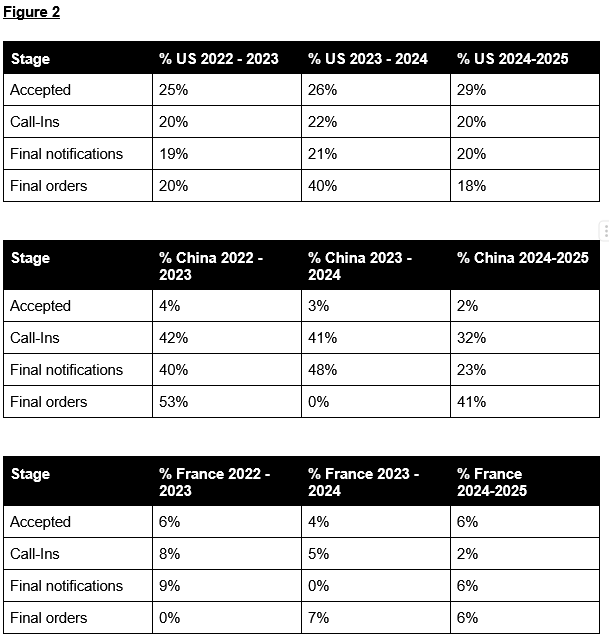

The NSIA’s investment review process functions as a funnel, progressively filtering investments from initial notification through call-ins to final orders. Figure 2 compares the process for US, Chinese, and French NSIA investments between 2022-25.

Viewed through this lens, US-origin investments emerge as a particularly stable, low-risk strategic source of investment in sensitive sectors of the UK economy. Figure 2 shows that although US investments have increased as a share of accepted notifications, they remain relatively unlikely to face escalation with final order rates fluctuating between 18-40%. In contrast, Chinese investments, though smaller in number, face significant scrutiny at multiple stages of the funnel: call-ins and final order frequently exceed 30-50%, suggesting their higher risk profile.

Comparisons with other allied investor nations, such as France, are more nuanced due to their smaller overall investment footprint. French investments indicate a similar low-risk pattern as US investments, albeit on a smaller scale. Overall, the funnel highlights not only the volume but the perceived reliability of US capital within the NSIA system: large in scale, steadily increasing, and comparatively unlikely to be the subject of government action as it moves through the review stages.

The future of US NSIA investments

The data examined above covers the Joe Biden administration and the first three months of the second administration of President Donald Trump. Looking ahead, US investments into sensitive sectors are likely to face greater scrutiny given the geopolitical context of changing US-Europe relations.

Two final orders issued in September and December 2025 involving US-backed investments into Oxford Ionics Limited and Oxford Nanoscience Limited, both quantum computing companies [LINK, LINK], provide an indication into the likely direction of travel.

In both cases, the remedies imposed as conditions of approval prioritised the maintenance of UK sovereign capability and the protection of supply chain and operational resilience for future UK government programmes requiring quantum technologies [LINK, LINK]. The NSIA order for the Oxford Nanoscience Limited acquisition further required that the UK government retain access to Oxford Nanoscience Limited technology on “reasonable commercial terms” [LINK].

Taken together with final orders with non-US origins of investments – where mitigations have included enhanced protective security measures to safeguard intellectual property [LINK], ownership restrictions [LINK], data access measures [LINK], and security vetting for board members [LINK] – the approach indicates a potential shift in regulatory pattern towards US investment. Instead of replicating the more defensive measures applied to strategic competitors like China, it indicates a more calibrated shift in how the UK adapts security measures to manage new geopolitical risk associated with US investment.

These mitigating measures align with wider strategic goals of decoupling from US technology dependence by maintaining and developing sovereign capabilities, while also reducing exposure to potential US leverage and pricing coercion; risks rendered more credible by the Trump administration’s increasingly transactional posture.

Scrutiny of US investments and mitigating measures are likely to be accelerated after the Trump administration’s aggressive demands for the Danish territory of Greenland in January 2026, resulting in vocal criticism by European leaders [LINK, LINK]. However, US investment is highly unlikely to disappear given that US capital operates at a scale that European investors struggle to match, especially for growth-stage and capital intensive technology [LINK]

Implications for organisations operating in NSIA-defined sensitive sectors

Likelihood of delays in reviews due to increased caseload for the Investment Security Unit (ISU).

As perceived geopolitical risk associated with US investment increases, NSIA reviews are likely to slow, with more US-linked transactions triggering deeper scrutiny and adding pressure to the ISU caseload.

Required mitigating measures for US investments are likely to change.

Mitigating measures are likely to increase and focus on safeguarding sovereign capability and fair pricing, designed to limit the risk of US investments being leveraged for political or economic pressure.

Increased scrutiny from investors and external observers of ‘NSIA readiness’ of US origin investment.

Investors and associated third-parties are likely to place additional scrutiny on organisations’ security governance and resilience to US geopolitical risk. European investors may seek to reduce operational dependence on US technologies.

Deal structure and governance will become more important

Legal and investment teams will likely need to incorporate NSIA resilience into deal structures and governance from the outset to manage US geopolitical risk rather than retrofitting mitigations post-notification.

For more on this issue:

NSIA 2024 - 2025 Annual Report Analysis [LINK].